Why You Need a Creative Financing Toolbox

Building your real estate investing portfolio is like crafting a custom home. You need a set of reliable and flexible tools in order to build a solid structure.

Like a hammer, traditional bank financing is a common tool that everyone knows how to use. And there’s nothing wrong with a hammer. If you have a nail, it sure is handy.

But I’m here to tell you that depending only upon bank financing for real estate investing is a handicap. It’s like building a house with one tool. It will limit your business over the long run.

Other investors with a larger toolbox that also includes creative financing will have a natural advantage against you. They will build their real estate portfolio faster, more consistently, and with a better long-term result.

Related: You Can Avoid After-Hours Phone Calls From Tenants—Here’s How

There are multiple reasons why this is true. I’ll explain just a few here.

Real Estate Cycles

Real estate markets go up and down, often in seven- to 10-year cycles. The best real estate deals are found during the down cycles. Think about 2008 to 2009 when blood was in the streets and good real estate deals were plentiful.

But guess what? Down cycles are when banks lend the least money. Even if you recognize good deals, your ability to buy them will be limited if you can’t borrow money. On the other hand, creative financing smooths out the curves of these cycles and works during up and down times.

For example, in the downturn of 2009, we were able to obtain plentiful private financing from individuals who were scared of the stock market and sick of tiny bank CD rates. At this time, when banks would not loan money against investment real estate, our private lenders felt very secure with tangible real estate that produced rent far in excess of their interest payment.

At the same time, many sellers couldn’t get rid of their properties. They were much more open to seller financing during the down cycle than they would have been before. So, rather than working against us, the down real estate cycle actually improved our ability to finance deals creatively.

Increased Risk

Do you know how you can tell that a bank is in control of your lending relationship? Because their army of attorneys wrote the enormous book of papers you sign at a loan closing. You get the privilege of signing the papers as-is, or you can take a hike!

That big stack of papers is all about transferring risk. The attorneys working for the bank essentially transfer as much risk as possible from the bank to you. The risk equation may be out of balance in the bank’s favor, but the terms are not negotiable.

On the other hand, everything is negotiable with creative financing. It’s possible to find win-win agreements with sellers, private individuals, or small businesses who are willing to finance to you. These agreements can reduce your personal risk and still satisfy the needs of the other party.

Lack of Control

Success in real estate investing depends upon consistently being able to acquire funding for new deals. But the application and approval process for bank financing is largely outside of your control. Today you may be able to get seven loans, but tomorrow the policy may change to five. And the changes do not always make sense.

On the other hand, creative financing is limited only by your ability to find good deals and to prove yourself to the individuals providing the financing. With your hustle and intelligence unleashed by creative financing, the potential upside of your investing business is virtually unlimited.

Lack of Speed

Ignoring all of the other problems above, bank loans are just too slow. For the best investment acquisitions, you must move very quickly. But bank loans require drawn out application processes, appraisals, and multiple layers of approval.

By the time you finish the first step of your traditional bank application, I will have already used creative financing to close the deal. For example, we recently closed a deal in three days. We would have been lucky to get a return call from the bank by the time we already bought the property!

The Basics of Creative Financing

Luckily, adding creative financing tools to your toolbox is not rocket science. You probably already know the basics. If you have used a promissory note, a mortgage, a deed of trust, or a lease, you understand the fundamentals of how creative financing works.

But there is still a learning curve to understand the nuances and the unique applications of these tools. Almost daily in the Divito Real Estate Group Forums, a newbie investor complains that a local closing attorney or title company refuses to close their creative financing deal or says that what they’re doing is illegal.

While I can empathize with the situation, my hunch is that most new investors really don’t understand the tool themselves. It’s like this closing attorney sees a small child climbing up to turn on a power saw. The attorney may not know how to use the power saw either, but he knows enough to scream, “Stop!” before the child cuts off his finger!

So, the goal of my explanations below is to make you more familiar with five of the most common and useful creative financing tools. I will share diagrams and examples that will explain how the tools are used.

I’ll begin to unpack these creative financing tools by explaining the tool you’re probably all familiar with: traditional bank financing.

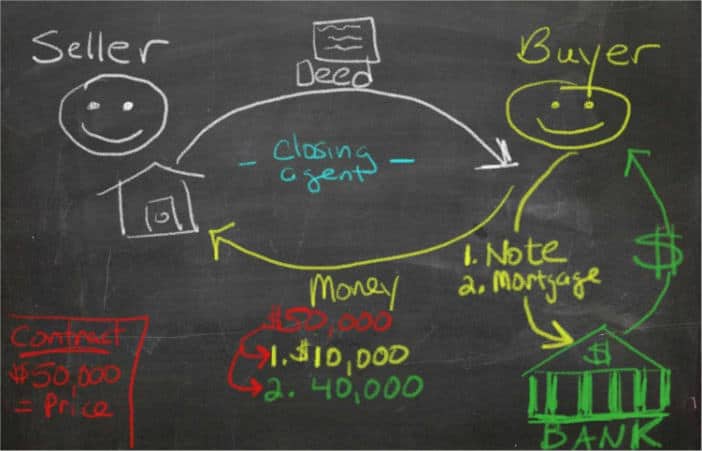

A Picture of a Traditionally Financed Closing

If you’re going to be able to understand creative financing and explain it to a skeptical attorney, real estate agent, or seller, you need to first understand each piece of a typical transaction.

The diagram above shows the relationship between all of the parties of a typical closing. There are four primary entities involved:

- The Seller

- The Buyer (you, if purchasing an investment)

- The Bank (lender)

- The Closing Agent (an attorney or title company)

In this example, a purchase and sale agreement was signed at some point before closing between the buyer and seller. The price was $50,000. Also before closing, a loan commitment agreement was made between the buyer and the bank. The loan was $40,000, and the buyer provided $10,000 or 20 percent as a down payment.

The closing attorney or title company uses these pre-closing agreements to oversee the closing transaction (aka escrow) to ensure the other three parties are treated fairly per the terms of their contracts. The items actually exchanged between the parties include:

- Money — from the bank to the buyer (a loan)

- Two contracts, a promissory note, and a mortgage (or deed of trust in some states) — from the buyer to the bank

- A deed — from the seller to the buyer

- Money — from the buyer to the seller

For those of you already investing, this may seem basic. But it’s important to start here before doing transactions that are a little more creative, because these creative tools use the same basic format.

Now I’ll unpack my five favorite creative financing power tools from my toolbox.

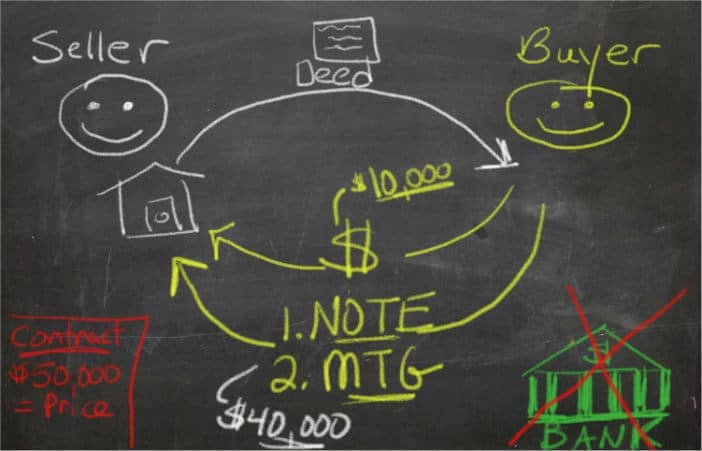

Power Tool #1: Seller Financing

In the picture above, did you notice the main difference between a seller financing transaction and a transaction with a bank loan? Obvious, right? There is no bank!

Related: How to Build a Credit Score From Scratch

In fact, technically, there is not even a loan. As you can see, the seller never gives the buyer any money like a bank would. Instead, the seller just agrees to let the buyer pay the purchase price over time with monthly installments (i.e., an installment sale).

In exchange for this financing arrangement, the seller (not a bank) receives the promissory note and mortgage as security.

The beauty of this arrangement is that there are only two parties—the buyer and the seller. The seller does not have loan committees, underwriters, or Fannie Mae-conforming rules. You make an offer to the seller, the two of you negotiate, and if it makes sense for both parties, you move forward.

But how common is seller financing, really? Well, Ben Leybovich, a well-known creative financing writer here on BP who I respect, once wrote that seller financing is rare and usually only used on ugly pig properties. While I normally nod my head at Ben’s articles, I shook my head and chuckled at this one. Maybe Ben has been looking under the wrong rocks.

It’s true that seller financing is not as common or as easy to obtain as more traditional tools. It’s also true that seller financing does not make a bad deal magically turn into gold. But don’t let its difficulty dissuade you from its ultimate value.

Seller financing is an incredible tool that is well worth the effort. And it is one of the clearest win-win transactions in the entire real estate business.

For example, my business recently bought an income property using seller financing with a 10 percent down payment (yes, in a hot market, and yes, in a desirable location). Once stabilized and rented, this property will likely make us over $1,000 per month in net income for decades to come. And that does not include the benefits of future capital gains.

What’s more? The seller and I are pals. He is happy as a clam in water because he loves monthly checks without the hassles of being a landlord. I have saved him the trouble of putting a big chunk of his money into investments like stocks or bank CDs that he doesn’t like or understand. And he receives a much larger income than he would with most traditional investments.

Who is the only party not happy with the transaction? I guess it’s the bank, who didn’t get my seller’s money in a CD, so that they could loan it to me at a higher interest rate!

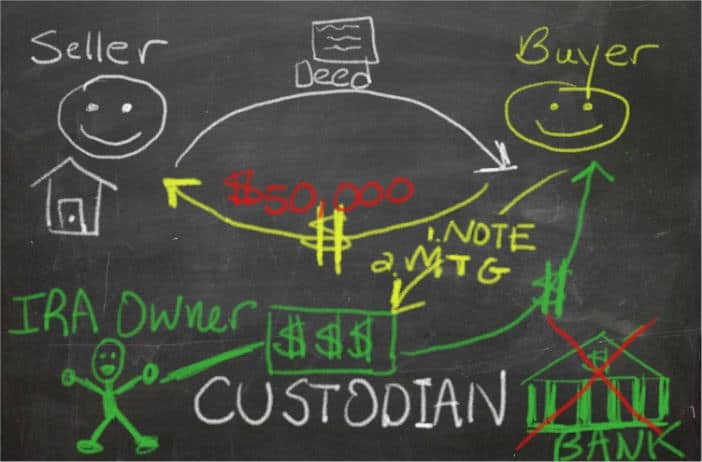

Power Tool #2: Private Loan From a Self-Directed IRA

As you see above, this creative financing tool is structurally very similar to a closing with a bank loan. The only difference is that the lender is a self-directed IRA (individual retirement account) and not a bank.

Most retirement accounts invest in traditional assets like mutual funds or bonds. But a self-directed IRA is a way to use retirement savings to invest in alternative assets like real estate, notes, tax liens, and more. Specialized custodians who allow self-direction hold the assets and process transactions and keep records for the IRS.

The point of this tool is to borrow the IRA funds from other individuals, not from your own IRA. You must be very careful not to engage in IRS-prohibited transactions. Loaning money to yourself or to your business is clearly off limits.

But as long as you follow the rules, you have enormous opportunities to find sources of funds for your real estate deals. Even a few years ago in 2012, total IRA accounts in the United States totaled over 5.68 TRILLION dollars!

Chances are that someone you know in your local network has funds available and would be willing to loan them to you. Some of the best candidates are other real estate investors who can’t loan that money to themselves. Your deals give them the perfect opportunity to invest in local assets that they know and understand.

This has been the tool that I use the most often from my creative financing toolbox. Like seller financing, it is a win-win arrangement. It gets you the funds you need, and your IRA lender receives a solid return and good collateral.

Related: Mortgage Consultation

Power Tool #3: Private Loans (Outside of an IRA)

I didn’t include a diagram here because it is the exact same process as the previous tool. The only difference is that the private lender uses funds outside of an IRA.

Who would have that kind of money? More people than you think.

The most likely candidate is an individual with a large net worth.

My favorite way to find these individuals is at real estate networking events. Attend these events and get to know people. Find the experienced old guys and gals in the back of the room. Ask questions. Make friends. Once you get to know people, they may be willing to loan money to you.

I love that borrowing from high net worth individuals also brings more benefits than just getting the money. In addition to borrowing money, you also borrow their expertise and experience!

A couple of my own private lenders became mentors and close advisors. While they may have been interested anyway, the fact that I had their money made them VERY interested in my success. Their tips, feedback, encouragement, and friendship over the years have been an essential part of my own success on their deals and on others.

While I personally have never used hard money loans, I would also lump hard money lending into this same creative financing tool. Hard money, or asset-backed loans, are an alternative to traditional bank financing. And while the cost is generally higher than normal, the availability and speed of funds make them very helpful to many investors.

Power Tool #4: Master Lease With Option to Buy

The tool of master leasing is where we begin to think outside the box even more. So, stay with me.

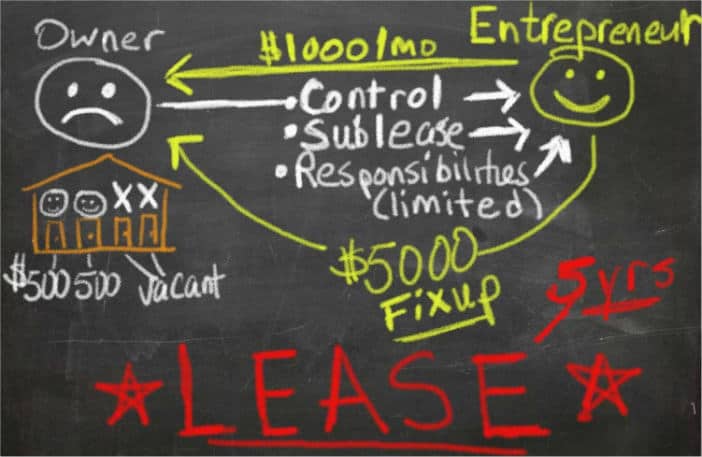

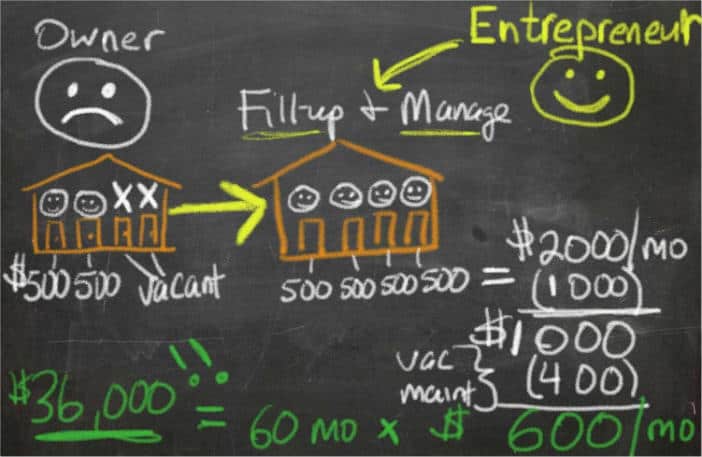

In the illustration above, a burned out landlord named Jane owns a quadruplex building. Jane has let the building run down, and she has not even filled two vacancies from bad tenants who recently moved out. She’s just too tired.

Jane then gets a letter from an energetic entrepreneur named Chris, who offers a creative solution to her problem. Chris offers to lease her building for five years for the same amount she currently receives in rent from two tenants ($1,000 per month). He also offers to perform immediate cosmetic repairs like painting and carpeting that will cost him $5,000.

Jane will continue to pay for taxes and insurance and handle any major capital expenses (roof, heat and air systems, structural issues). Chris will be responsible for all vacancy costs, turnover costs, maintenance costs, etc.

Because Chris’s lease gives him the right to sublease all four units to sub-tenants, his gross rent collected in this case is $2,000. As you can see in the picture below, if his vacancy and maintenance expenses are $400 per month, he receives positive cash flow of $600 per month—or $36,000 over the next five years!

Stacking up a few deals like this could make for very lucrative side income for Chris, or he could really ramp it up with more deals to completely replace his income from a job.

But why stop there? Let’s see if Chris can make it even better using another tool: the option to buy.

If Jane, the burned out quadruplex landlord, was willing to give Chris, the entrepreneur, a master lease, might she also be willing to give him an option to buy the property? There’s a good chance.

An option would essentially give Chris the right (but not the obligation) to purchase the property for a set price for a certain period of time. In exchange, Jane receives consideration for selling him the option.

In this case, Chris’s consideration is the $5,000 he spends to spruce up the cosmetics of the property. Jane will give him a credit in the amount of $5,000 when he finally executes his option.

Chris’s option strike price is $120,000. Once he gets the building rented and looking good, he then will have the chance to make money from the option any time during his five-year option window.

Multiple Exit Strategies With Options

A well-crafted option gives Chris at least three profitable exit strategies:

- First, Chris could patiently save a down payment and look for permanent financing and/or partners. This will allow him to buy the building and keep it as a long-term hold investment. Because he has five years to accomplish this, he can shop around until he finds the best terms.

- Second, Chris could use this as the replacement property in a 1031 exchange. This would allow him to sell another rental property he owns, exchange into this property, and defer his taxes on the gain of the sale. Given that many investors don’t have the perfect property picked out when they execute a 1031 exchange, this can be a BIG benefit.

- Third, Chris could sell his option to another investor. Let’s say he finds a landlord investor, who is willing to buy this property for $160,000. He could simply assign his option contract to him (yes, contracts can be sold), and his fee for the assignment would be the difference between $160,000 and his strike price of $120,000—or $40,000.

So, in addition to the $36,000 Chris earns from operating the rental over five years, he also receives a profit of $35,000 ($40,000 minus the $5,000 initial investment) from assigning his contract.

That’s a total of $71,000! Not a bad payday considering he invested only $5,000, some hard work, and a little creativity.

And perhaps even more exciting than the $71,000 profit, the lease option allowed Chris to use enormous leverage without the typically enormous risk of traditional bank financing.

Remember the bank’s army of attorneys I wrote about earlier? If things go badly with Chris’s lease option, he has only risked his $5,000 initial investment, his time and energy, and any potential negative cash flow during the five years of his lease. After that, he could legally just walk away.

Related: Ask a real estate pro: Who has to pay for window broken by stray golf ball?

Try that with a bank loan!

Power Tool #5: Master Lease + Option (With a Credit Partner)

If you liked master leases and options with sellers, this next tool will give you a different way to use the same technique. Instead of lease optioning the property from a seller, you lease option it from a credit partner.

Let me explain.

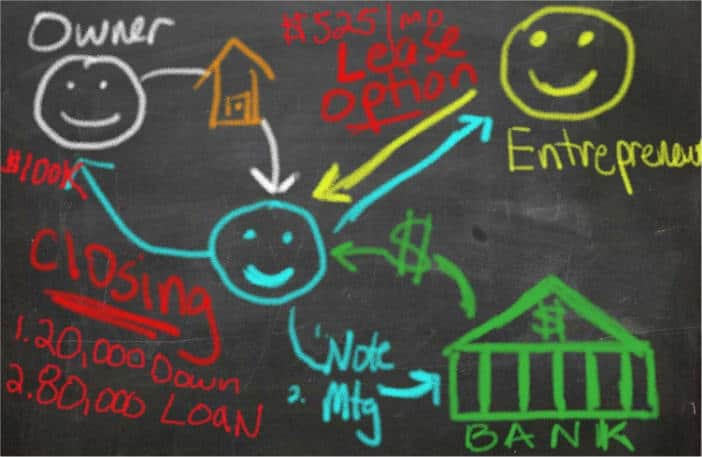

Let’s say an entrepreneur named Karla finds a great rental property deal worth $150,000 that can be bought for $100,000. The only problem is that she doesn’t have the money to close. She knows a private lender named Jim with $20,000 cash, but obviously that’s not enough.

After further questioning, Karla learns that Jim does have excellent credit and can get a mortgage loan. So, the two of them agree to the following:

- Karla, the entrepreneur, assigns the purchase contract to Jim, the credit partner.

- Jim applies for a traditional bank loan and purchases the property for $100,000.

- Karla immediately master leases the property for 5 years at $525 per month net-net-net rent (i.e., she pays all expenses).

- She also retains an option to repurchase at a higher price ($110,000).

- She manages the rental until future exit strategies are available.

Karla then proceeds to rent to a sub-tenant for $1,200 per month. Her net income looks something like this:

$1,200 – $500 (operating expenses) – $525 (rent) = $175 per month net income

While $175 seems like a nice cash flow, Karla will be wise to set aside a good portion of her cash in reserve for capital expenses and vacancies.

Meanwhile, Jim uses the $525 rent from Karla to pay his $425 mortgage payment, and he still has $100 left over to put in his pocket.

Another Option, Another Profitable Exit Strategy

Just like the lease option example with the seller, Karla has multiple options for exit strategies, including refinancing, 1031 exchanging, or assigning. The choice she makes will depend on the circumstances and resources available to her at the time.

But what if this property has great long-term prospects? What if Karla can’t obtain long-term financing? What if both parties want to stay in the deal together as partners?

To accomplish this, they could make a slightly different credit partner arrangement.

Jim could give Karla an option for 20 years instead of five. But instead of an option for 100 percent of the property, Karla retains an option to purchase a 50 percent interest in the property at 50 percent of the original purchase price.

In this case, Karla would pay $50,000 to Jim whenever the option is executed. Jim would then deed a 50 percent free-and-clear interest in the property to Karla, or he could sell her 50 percent in an LLC if that makes more sense.

Why would either party do this? Because perhaps this location is prime, and 20 years from now, the property could appreciate from $150,000 to $400,000. And during that time, perhaps the rents could increase significantly for Karla, and the loan will certainly keep getting paid down for Jim.

At year 20, Jim has used the rents from Karla to pay down his loan from $80,000 to $40,000. So, his 50 percent portion of the equity in the property is now worth $200,000 minus $40,000, or $160,000.

Karla, on the other hand, controls $150,000 of equity ($200,000 minus $50,000 option price), but she has yet to put up any capital. As before, she again has multiple exit options.

If Jim wants to, Karla could refinance and buy out Jim’s equity of $200,000. Or Karla could sell her equity to Jim for $150,000 cash. Or if both partners want to cash out, they can just sell the property and divide their winnings.

In the end, Jim turned $20,000 into $160,000 completely passively, and he also received $1,200 in rental income for 20 years. It’s very likely his income was completely sheltered by the depreciation of the property, meaning he paid very little in taxes until the sale.

For a bonus exercise, do the math on Jim’s internal rate of return (IRR). I’ll give you a clue that it’s better than he’d get historically in the stock market.

Karla invested zero money up front, and she used her creativity and property management skills to accumulate $150,000 of wealth. And along the way, she built a steadily growing stream of positive monthly income.

And because I know how smart and ambitious Karla is, she probably did another nine deals just like this so that after 20 years, she created over $1.5 million in wealth and thousands of dollars in cash flow per month.

Aren’t these power tools fun?!

What Tools Are in YOUR Toolbox?

As I said way back in the very beginning, these are tools my business partner and I have used over the years in our own business. They have served us well. Our toolbox and our tools are well worn now.

But the point of the article is about you. The question is, can you use any of these tools to build wealth and income for yourself?

My advice is not to fill up your toolbox with too many tools at once. It’ll just weigh you down unnecessarily.

And you don’t need to give up your old tools, even the hammer of traditional financing. If it’s already working for you, keep using it.

Instead, decide on one or two of these tools that you’d like to add to your toolbox. Then commit to mastering that tool.

Learn about it. Practice it. Ask questions. Then, as quickly as possible, start using the tool in your real estate investing.

I think you’ll become a better and wealthier real estate investor as a result. Best of luck!

Bigger Pockets